18 months since - funding statistics for the 2021 space startup cohort

18 months has been long regarded as a proxy for how long a runway should a funding round provide. The end of Q2 just marked 18 months since the end of 2021 - and I coincidentally track space startup investments since then. Looking at funding rounds from a backsight is incredibly important, helping us to turn dots into lines and begin to understand how space investments transpire over time.

The first part of this article centres on numbers and their adjacent context - providing the raw number figures and discussing the data collection and limitations. If you are more of a words person - the second part is for you, building upon the numbers and adding much-needed context at the intersection of space, finance and strategy.

Raw data

My database tracks 93 space companies which received an investment in 2021. Geographically, over 40% of startups in the set are US entities, followed by Japan, the UK, Canada, India and Australia.

In 2021, they received a total of 4.75B in funding, but without the two biggest rounds (Relativity Space and Sierra Space), the adjusted number is closer to 2.7B USD.

Till the end of Q2 2023, those same set of entities received a further 1.8B in investments.

48% of space startups which received an investment in 2021 attracted further funding.

28 companies in total announced an investment round larger than the 2021 one. That makes 30% of all companies in the cohort and ⅔ of the companies which did receive a new round of funding.

26 of the companies have a significant overlap of the existing investors in their new round - 19 of those matches also fall into the “larger new round” category, so those numbers appear to be correlated

In 2021, 17 rounds have been over 50M in size in contrast to 11 for the same cohort since then.

The median period between investment rounds is 17 months, regardless of outliers. The average would jump slightly by 25 days to 18.2 months if we remove 3 rounds which happened within 12 months from the first one.

Lyteloop, Porkchop, Hiber, Vorb, Sky and Space Global, SpaceLink left us since. May you rest in peace. Special mention to SpaceIL which is not a VC-backed organisation.

Launcher got acquired since and iSpace went public.

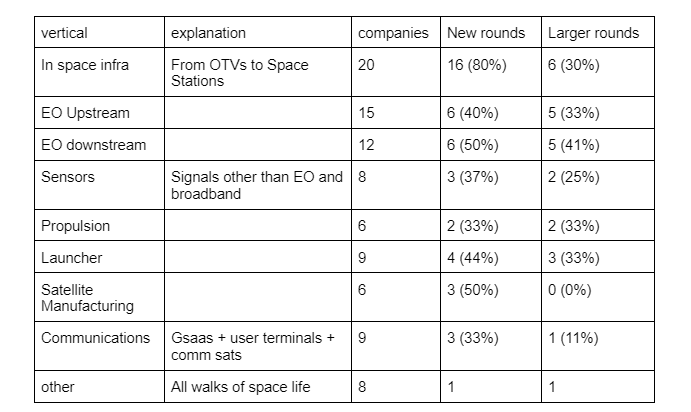

For specific verticals, the numbers look as follows

The dataset

The above raw numbers are based on my proprietary database. I took a set of companies which received investment in 2021, mostly covered in the 2021 Space Funding Dynamics Report. The 2021 edition omits two important categories - satcom user terminals and SSA companies - I made sure to add them to the database. For the set of companies, I collect the date & amount for the 2021 round and the same for the next major subsequent round.

My database ignores companies in China and large equity rounds for SpaceX/OneWeb, under indexes geospatial downstream and works mostly only with publicly announced rounds. I decided to include rounds for Leaf Space and HE360 even tho they happened in July. On the other hand, I mostly do not include government funding matching. There are a lot of deliberate choices to be made when assembling a database - I always tried doing them to make the final answer more telling. Please bear the law of small numbers when interpreting the data.

The dataset will of course become more valuable over time.

At the end of this year and mid-next year, enough time will pass to see how the new cohorts of companies performed. A lot has been said about the funding trends over the last three years (2021-bubble at its peak; 2022- market downturn; 2023- market correction). I’m really interested in how this translates into the subsequent funding numbers.

In this edition, I use a simple average for a time in between rounds. For the next edition, I shall change that into percentages for each cohort - so it would look something like “5% of companies got an investment within a year; 15% within 15 months; 20% w/o 18 months; 15%... and so on (numbers made up); + outflows into public markets, acquisition and bankruptcies.

Commenting on the figures one by one

Significance of the statistical sample

For the 2021 period, BryceTech Startup Space 2022 report suggests 212 investment recipients. That is significantly more than my set of 93 companies. The difference will cause partially by disclosed choices (only public rounds above 1M, ignoring add-ons and Chinese companies) and some by the limited quality of my data collection. While the 93 figure is not exhaustive, it contains a large enough proportion of relevant rounds to give significant answers.

The difference is addressed volume between 2021 and subsequent rounds

Statistically, the 900M difference in funding for the two cohorts does not have a clear-cut explanation - it's really a difference between them. It is caused both by larger rounds (difference of 6 rounds with a minimum size of 50, which is at least 300M) and approx. 50 transactions with a median value of 10.5M without a subsequent round. The change must be explained at least partially by the macro environment - but this type of analysis can confirm only after the next few editions are available.

The probability of subsequent rounds

50% of subsequent investments w/o 30-18 months is an easy-to-reference figure and a much more useful number than a poorly defined 90% startup failure rate. 30% of larger rounds is a surprisingly small figure over me. While many of those have clear explanations, startup financial/outcome modelling absolutely fundamentally lies on increasing round sizes - at least up to series B/C and I cannot imagine how those might translate into internal operations decisions.

Loyal investor base

A large correlation between subsequent rounds and a loyal investor base is more of a US phenomenon followed loosely around the world. For startups, this suggests to look for investors able to chip in the next rounds if possible. On the other hand, that depends on the tradition of multi-stage funds in any given regional investor base, so it may be less critical than appears from the data.

Time in between rounds

The median time since the investment and the end of Q2 2023 for companies which did not receive an investment is 22 months. So it is distinctly higher than the median time in between investment rounds for this cohort. On the other hand, the set of companies which did receive the investment has also a second peak between 20 and 23 months. So it is important to bear in mind that while the 18 months since is indicative, it is not necessarily yet predicting company failures.

Low optionality for space infrastructure companies

As for specific verticals, it is really interesting to see space infrastructure topping the leaderboard of subsequent investments. My explaining thesis centres around optionality. With a worsening funding environment, companies from other verticals have a higher degree of choice in pursuing other objectives and delay fundraising. Typically, an upstream EO company may decide to delay further satellite launches, focus on high-end imagery customers, work on related software and accelerate the hardware development once the funding environment becomes more friendly. On the other hand space infrastructure companies, like commercial space station operators do not have much choice but to continue capital-intensive activities and thus needed fundraising.

Please note that the vertical-specific taxonomy is more opportunistic and distinct from the industry convention.

Cash is the king

Space companies need A LOT of cash to run. If a space company doesn’t announce a round within 18 months, the assumption to make that cash must have flown some other way - but there is simply no scenario in which the company is surviving without another source of cash.

The best and underappreciated scenario is where a company earns enough revenue from the service it provides so no further external financing is needed. I cannot guess for how many of the companies in the set is the case. It is certainly possible for asset-light businesses - for example, both HEO Robotics and RBC Signals suggested to be profitable before their somewhat opportunistic rounds in 2021.

There are a couple of points to note. Paradoxly, if a company generates sustainable revenue, it actually makes it more attractive to investors who in turn offer more appealing conditions increasing the incentive to take an external source of funding. Second, I will discuss it later in this section - but investors and founders might not (are not) aligned on incentives. And so even if a company could generate sustainable profit, the board will likely push to aim for more ambitious targets at higher valuations at the cost of taking external money.

A variation to revenues as a source of funding are large government contracts. For some companies, that is the primary customer, for others it might be not. While its last funding round happened in mid-2021, Gilmour Aerospace, an Australian launcher has since received 15M AUD from Australian DoD and 52M AUD funding for facilities development. That together obviously delays the necessity of a new investment round.

Two sorts of technical reasons come back to the investment rounds. While I was able to catch some undisclosed rounds, a simple reason why a company appears without a subsequent round might be the round has happened but was not publicly announced. Two recent undisclosed rounds are for example Umbra’s series B and Varda’s pre-series C. Those still attracted some attention so I have listed at least dates. But for many smaller companies, the situation might be the existing investors will commit to an undisclosed bridge round to ramp up initiatives leading to a larger announced round.

The other technical reason might be the round is well in progress and the announcement will come up soon. I have poked around Leaf Space on different occasions - their last round was closed in early 2021 so it was clear new funding must come at some point. Last month Leaf announced a 20M EUR investment round so the assumption was true.

The last still technical reason might be another source of financing. Excluding revenues, government and equity investments, debt is the last reasonable option and often companies might not publish it. I have included Astroscale’s series G round - about a month later the company also announced a major debt intake.

And of course, if a company doesn’t have a substantial other source of funding and there isn’t a visibility for a major new funding round, companies are on a trajectory which will result in bankruptcy. I wrote a whole article on the failures of space companies. Relatively few space companies end their lives with a firework show - especially for the smaller firms, employees will gradually leave realizing their stock options are effectively worthless, leaving some executives and a loyal circle trying to resuscitate the company.

I tried to run a very quick and biased guesswork to understand the proportion of different of these factors.

Investors want new rounds too - Markups & Institutional memory

Quantum physics and funding rounds share an interesting duality. The increase of the value of a company is continuous if you don’t look but becomes very discretionary with investment rounds. I have a personal example here. Golem invested in Odin Space towards the end of the last year. After the last SpaceX Transporter mission, Odin announced they have successfully tested their sensor in space. The quiz question - has the valuation increased?

Intrinsically - definitely yes. Practically, it is more complicated than that. Odin is now much more valuable than when we invested - but there is no way for me to prove that until the new funding round anchors that valuation - so I can markup my portfolio.

Those markups are incredibly important. Traditional VC funds might have a time horizon of 10 years. Within the first 3 years, most of the capital will probably be deployed and afterwards, the General Partners (those who run VCs) are likely to decide to raise another fund (Fund II) to continue to deploy while simultaneously managing the previous one and after three years or so the cycle might continue. GPs are broadly split into two categories - emerging and established managers.

Until probably fund III, the LPs (Limited Partners, investors into funds) have really no tool to evaluate whether GPs are doing their job well - sometimes only after the ten years of the first fund returns can be distributed back to LPs - but the VC firm can meanwhile be at their Fund 3 or 4.

Now coming back to the topic - most of the GPs in space are emerging managers, simply because the investment category doesn’t really exist for long enough. And until the first funds produce actual returns in cash, one of the few ways for GPs to demonstrate performance is to show VC markups. And, you have guessed it, without subsequent funding rounds, there are no markups to show.

It is good to remember that institutional memory goes a long way. Every time a financial institution places a wrong bet (on a space company) it might take many years to eventually come back to space investing. While it says little, most of the investors in planetary resources did not come back so far. 50% of subsequent funding rounds is not a bad score in my opinion - but if the current (let’s say 2018-2021) batch of startups doesn’t deliver promising results, it might delay progress in the space economy again. And of course, markups are a sign of it.

Downrounds

The sole presence of a funding round doesn’t tell us much about its relative success. Down rounds have been a big topic of the past two years and in an edge case, my interpretation of the data could be entirely wrong. Would we be to assume that all of the investments were down rounds, the winners would actually be companies which raised enough cash pre-2022 and avoided fundraising by now.

That said, I think this interpretation is unlikely to be true. From the few companies which announced valuations publicly it was either an increase (Fleet Space Technologies) or more or less flat (Astranis). For a lot of companies - especially smaller/European, down round don’t really work mathematically due to previous valuation and the newly raised amount. So while there were a few down rounds, I think the number was smaller than suggested by the media.

Continuous rounds

One day I will write a rant “Why we can never have a perfect fundraising data”. One of the elements greatly complicating the data collection are continuous rounds. In theory, funding rounds should be very discrete events. A new funding round gets opened, commits are collected, a term sheet is received, commits are exercised, and the round is closed, wired and announced.

The reality is much more spread. Some investors like to do pre-rounds (the access to founders and internal data is much stronger with some money in the company’s treasury). That is especially popular among corporate investors (think Hanwha & Kymeta; Boryung & Axiom; maybe also 8090 Industries & OrbitFab). For some types of rounds, early commits can be wired in advance. Then, a press release sometimes goes out, and the last spots in the round get filled. Some long-DD investors then glue their contributions on tops and early no turn to yes in a sight of an oversubscribed round.

As much as possible, I tried to sum up all of these continuos funding under one discrete round, but reality is more complicated than that.

Step up the PR game

When I start writing this analysis, my intention was also to put together some quazi-objective data point of “signal strength”. The idea is that while I cannot access the internal financial results a mix of signals (launched satellites, funding, hiring, media engagement) could produce some power ranking. One astonishing realization is how poor is the PR activity of some companies.

Now, I know PR isn’t, unlike making money, something companies need to do. But I cannot get over the fact some companies literary did not produce any valuable piece of news since their funding round two years ago. So one actionable takeaway from this article - please step up your PR game.

What am I trying to do?

Last five years I tried to understand, what is this space economy thing all about. In the sea of contradictory tendencies, raw figures like 400B space economy make wonders. I hope my contribution will be to have those numbers less made up. Once we have actual figures, we can start having the discussion on whether this is a positive or negative development and how to perhaps increase the number of subsequent funding rounds.

Every year a number of space VC transactions get collected. The number falls somewhere between 80 and 200 and if you also include Uber and Tinder because they use GNSS - you can make a slide in your fundraising deck that *SPACE IS REALLY BIG*. But turns out that is not an interesting story. What matters more over time is that the startup moves from the first check and lab testing the tech, then building its first satellites and then getting to the first million of revenue. Bringing in more capital, scaling the tech, growing revenues and hiring more people, transitioning into a real company and exiting and returning money to investors and showing it is possible. And somewhat, that is not shown until we have the data over time.

So my agenda overall is 1) bring better data to have a more quality discussion about this whole space business thing 2) have space companies better use finance industry tools 3) beam investment activity towards space businesses addressing large-scale terrestrial markets. And every time I say or do or write something, it really comes back to those three points.

Epilogue

There is just so much more I’d like to write on this topic. But then the article would never see the light of day. My favourite sad story from 2021 is about LyteLoop raising 40M. How quickly did we forget? It played a convenient role in statistics about the big space economy, but where is LyteLoop today? I hope that coming back to the transactions I distinctly remember with the benefit of two more years around helps me make better assessments of what’s about to happen.

Thank you for reading! As always, you can share your thoughts on LinkedIn, Twitter and me@filipkocian.com